Targets missed

As we look to the Autumn Statement and new official forecasts on Wednesday, it is worth having a look at where we got to in March this year, at the time of the Budget.

The Conservative-LibDem government had already failed significantly on deficit reduction compared with its original targets, as the snapshots below show.

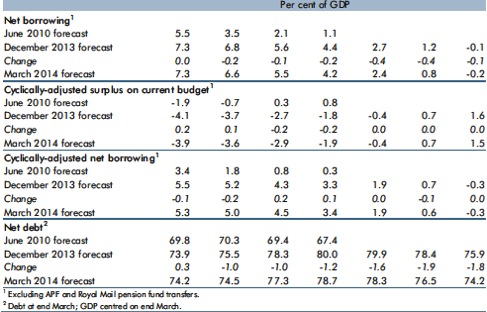

From the March 2014 Economic and Fiscal Outlook (looking at the Cyclically-adjusted surplus on current budget and Net debt):

The Cyclically adjusted surplus is supposed to be in balance on a five year rolling period. In 2010, that mean by 2015-16. It was forecast in June 2010 to be able to do this. However, the forecast at the Budget this year was substantially different - the government will miss that original forecast, though on a give year rolling basis (ie a moving target) it is on course (if a couple of years too late).

The supplementary target is for net debt as a % of GDP to be falling by the end of the parliament ie between 2014-15 and 2015-16. On the June 2010 forecast it does this, just. The revised March 2014 forecast shows net debt to be much higher as a proportion of GDP and rising (it only just falls in 2016-17).

When the net debt figure, expressed above as a % of GDP, is shown in £bn terms, we can see by how much the original forecasts have been missed:

For the current fiscal year, that amounts to £71bn more debt than planned, and in the next year the government will have borrowed £123bn more than it planned in June 2010 when it accused Labour of fiscal prolifigacy.

Finally, a look at the net borrowing figure is worthwhile:

This year (2014-15), net borrowing by the government is expected to be £58bn more than planned in June 2010.

The figures out this week will be notable for the effect of an expected upward revision to GDP forecasts and a downward revision to tax receipts, but the number of moving parts means predicting what the OBR itself will predict is impossible with any precision.

Stephen Beer, 30/11/2014